Various studies and articles claim that the health insurance market in India has great opportunities to expand further. However, they also agree on the common factor that there are many factors that are playing a direct and indirect role in hindering the insurance market to reach its potential.

The Economic Times article titled “Cancer care is expensive” mentions that there is massive misinformation and underperformance about and in the health insurance sector respectively. There are large assumptions stating that health insurance is expensive, and that few NCDs such as Cancer is genetic and inevitably lead to death. These assumptions, coupled with low financial literacy and low awareness are the reasons behind low penetration in India.

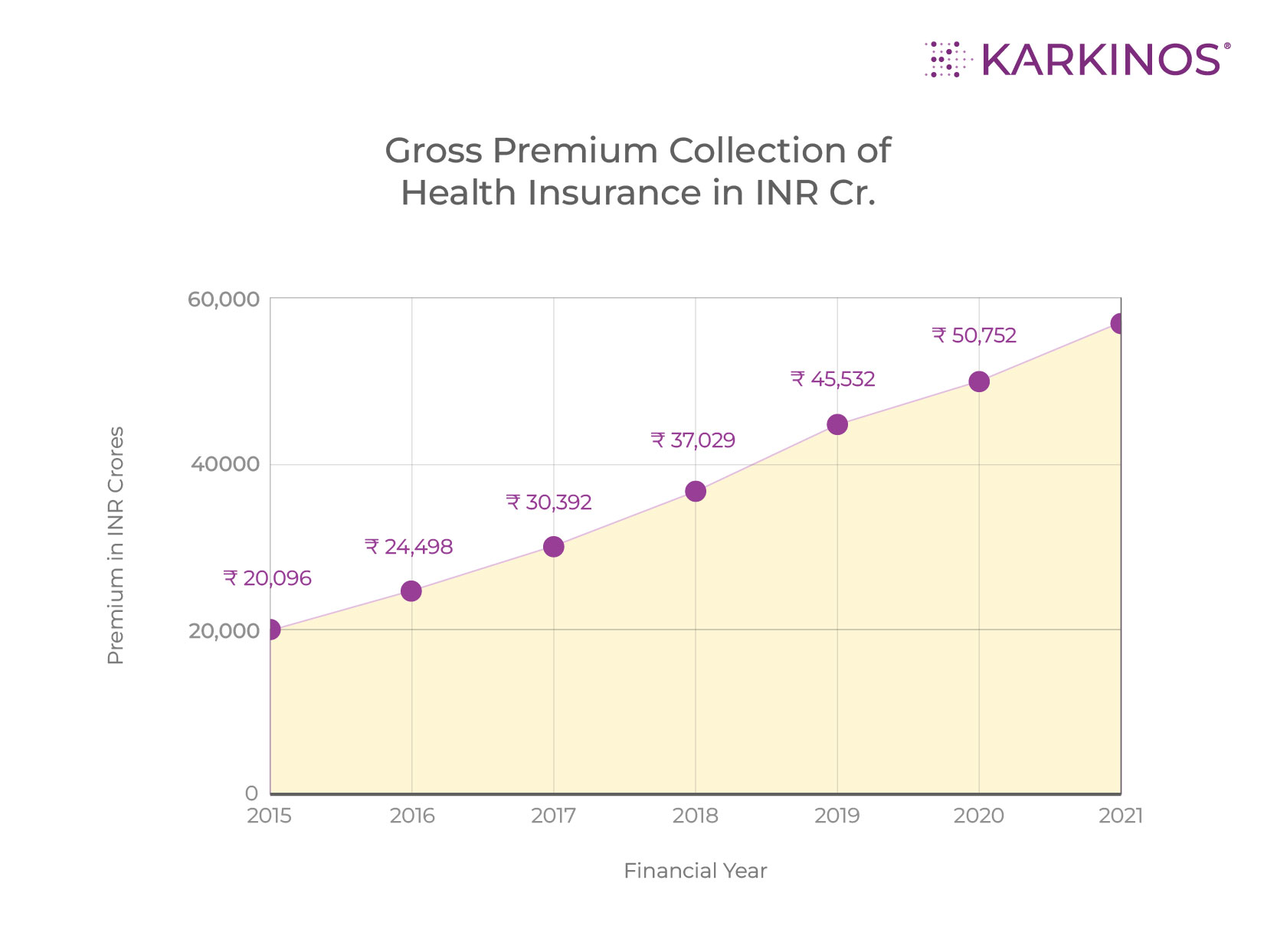

These observations are also seen in the health insurance market analysis paper by Dutta (2020) “Health Insurance sector in India: An analysis of its performance”.

A SWOT and PEST analysis reveals that the most prevalent weakness in the market stems from low investment. The public sector insurance providers are still preferred largely over private sector players due to higher affordability and better coverage and solutions. The additional fact of the service tax being increased on premiums, to a staggering 18%, is not benefitting the public in terms of affordability. There is also an increasing high claim ratio, which also includes an increasing number of false claims. With a rise in population of the younger generation, there is no increase in the adoption rates.

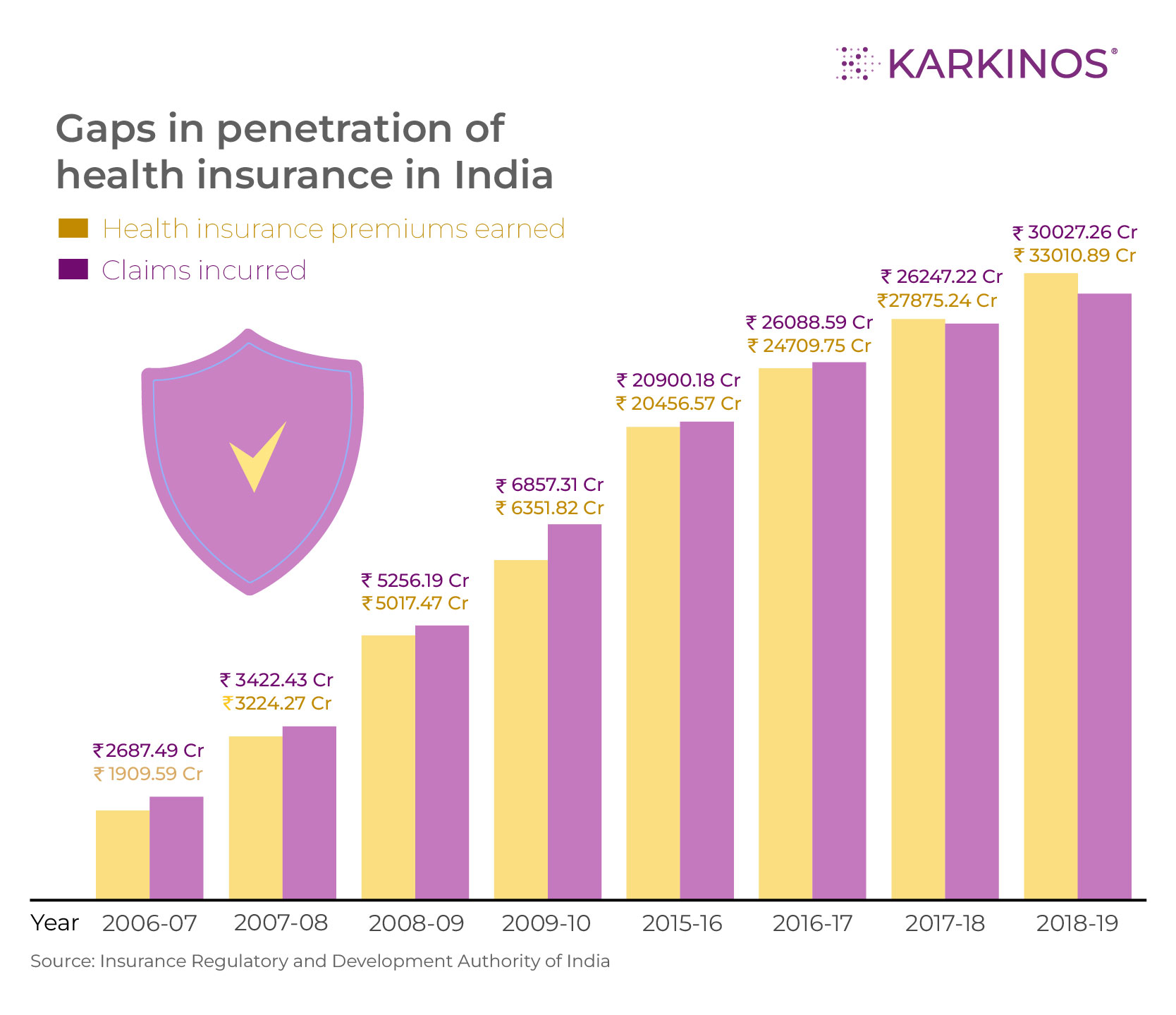

The data from Insurance Regulatory and Development Authority of India shows the following disparity between premiums earned and claims incurred:

The shadow of cancer casts a long and expensive reach, leaving many facing financial burdens alongside their health struggles. While traditional health insurance offers a safety net, it may not be enough to withstand the onslaught of costs associated with specialised cancer treatments. The limitation of traditional health insurance is that standard plans offer basic coverage but may fall short for cancer’s complex and expensive treatments.

Cancer’s Growing Threat:

- Cancer’s impact transcends borders, affecting millions globally.

- Diagnosis and treatment inflict emotional and financial strain on patients and families.

- The financial burden is particularly heavy for primary breadwinners, potentially jeopardizing savings and family stability.

- India’s rising cancer cases (20 lakh annually, 7 lakh deaths) highlight the need for specialised coverage beyond traditional health insurance.

Benefits of Cancer Cover:

- Targeted Focus: Covers various cancer stages, treatments, and related expenses.

- Financial Safeguard: Addresses high-cost treatments like surgery, chemotherapy, and radiation.

- Income Replacement: Provides crucial financial support during treatment-induced income disruptions.

- Holistic Support: Covers rehabilitation, counselling, and wellness programmes for comprehensive care.

- Global Coverage: Some plans offer flexibility for seeking international treatments.

- Early Detection: Encourages and covers regular screenings, crucial for improved outcomes.

Securing coverage for pre-existing cancer can be challenging due to higher risks. However, insurers are offering specialised plans catering to such individuals. These plans cover diagnostic tests, treatment, and post-treatment care. Careful evaluation of terms and conditions is crucial.

However, due to a lack of awareness and education about health insurance coverage, individual research on this is difficult (Why Cancer Cover in Health Insurance Matters More Than You Think, n.d.).

Factors to Consider When Choosing a Comprehensive Health Insurance Plan:

Focus on the scope of coverage and ensure it includes room rent, doctor fees, surgery, pre/post-hospitalization expenses, daycare procedures, diagnostics, and even critical illness riders or alternative therapies if needed. Consider the sum insured and tailor it to age, medical history, family background, and expected inflation to avoid out-of-pocket costs.

Network matters since it is essential to prioritise plans with a wide network of hospitals, cashless hospitalization options, and a proven track record for claim settlement. Claim settlement ratio and industry comparisons offer valuable insights into the insurer’s efficiency in settling claims.

Explore add-on benefits like ambulance coverage, OPD services, and wellness programmes that can enhance the plan’s value. Premiums, co-pays, deductibles, waiting periods, and renewal clauses are advised. It is important to understand these financial aspects to ensure affordability and avoid unexpected costs (Ray, 2024).

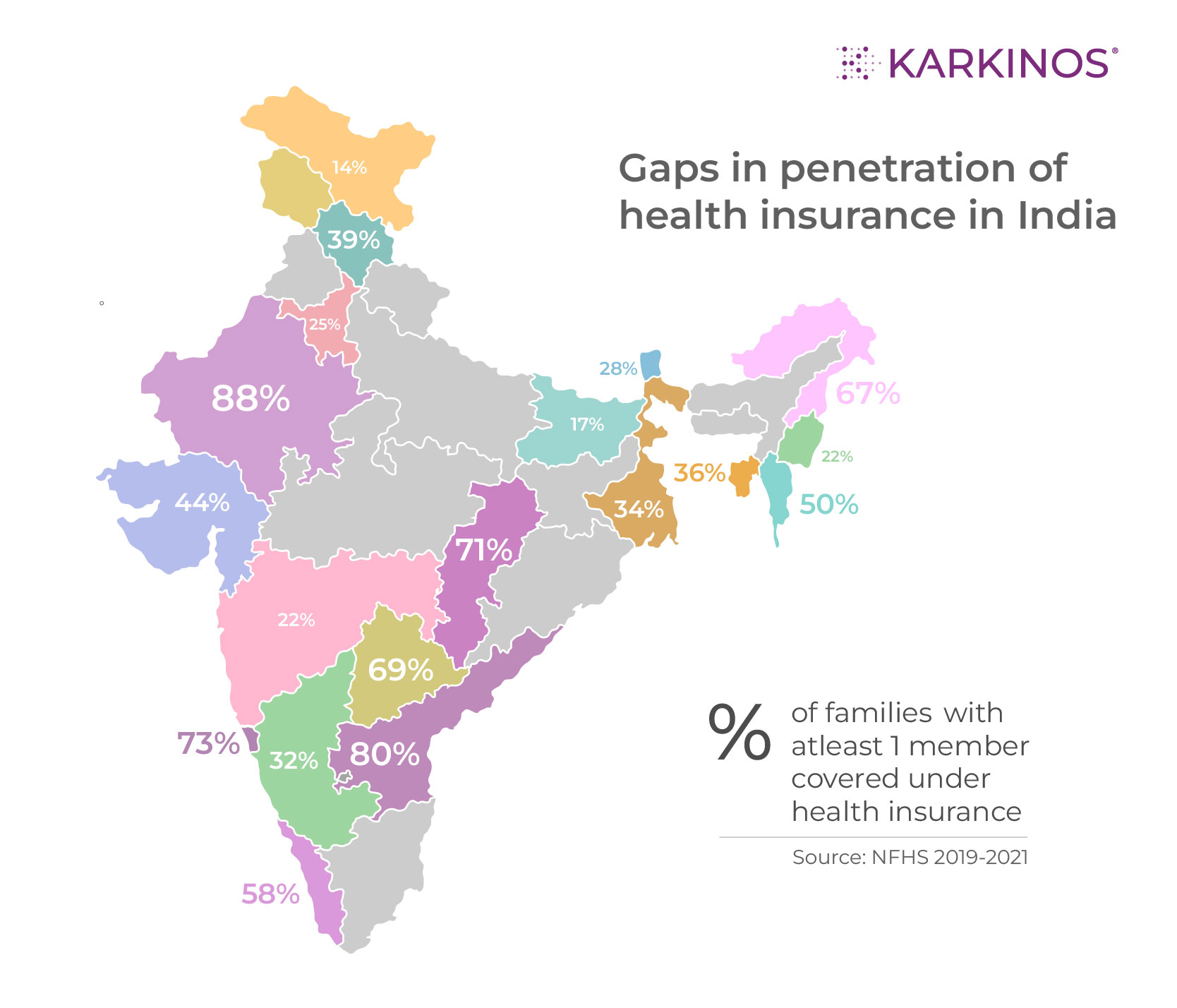

Cancer is a major public health burden in India. It is expensive to treat, potentially crippling finances and impacting families. Health insurance penetration in India is one of the lowest in the world, leaving many vulnerable (Spotlight, 2023).

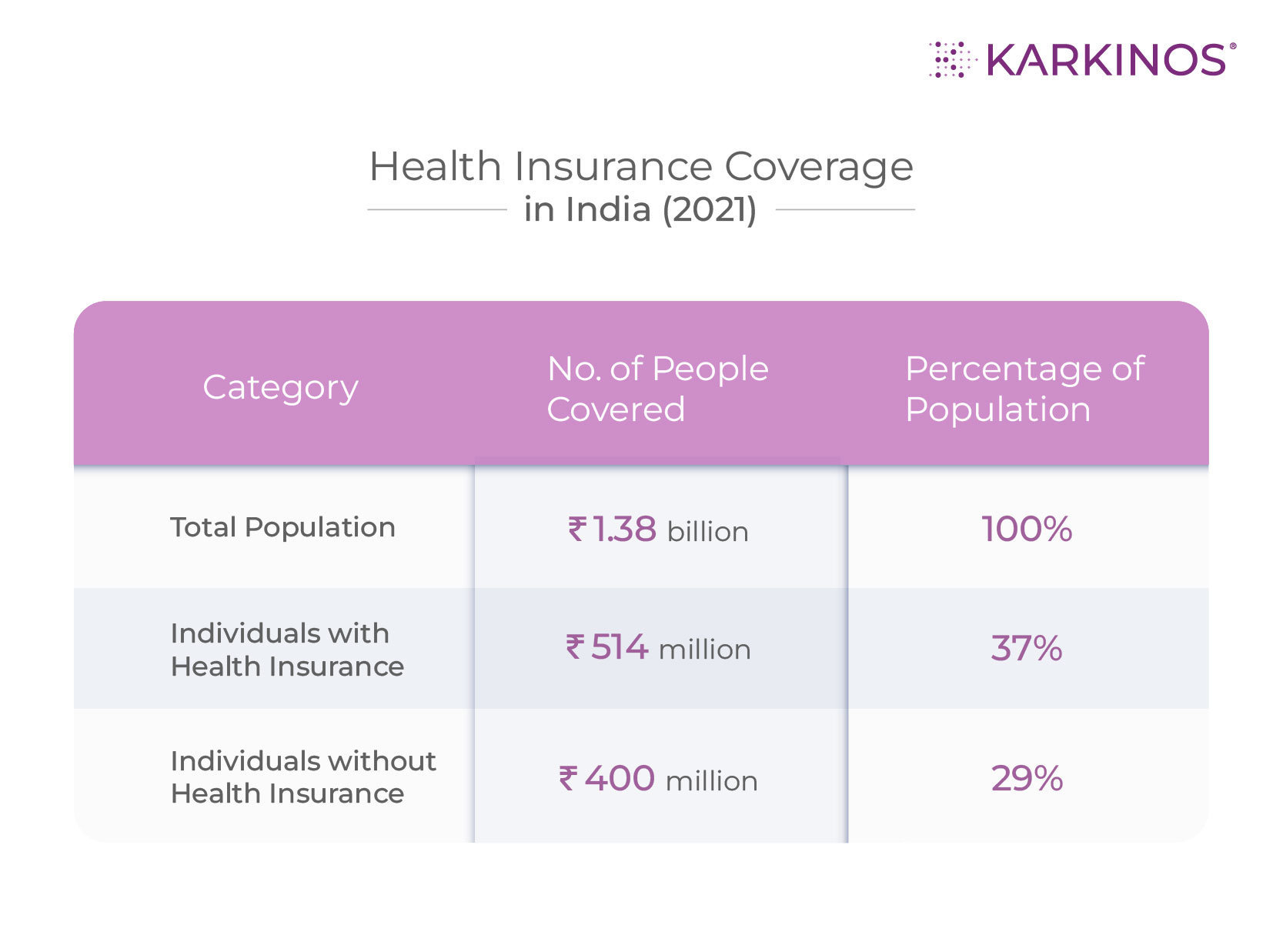

Despite the boom in India’s healthcare sector, fueled by government support, a stark reality remains – health insurance coverage is woefully inadequate. Only 37% of Indians have this crucial safety net, leaving a staggering 400 million vulnerable to financial burdens in the face of medical emergencies.

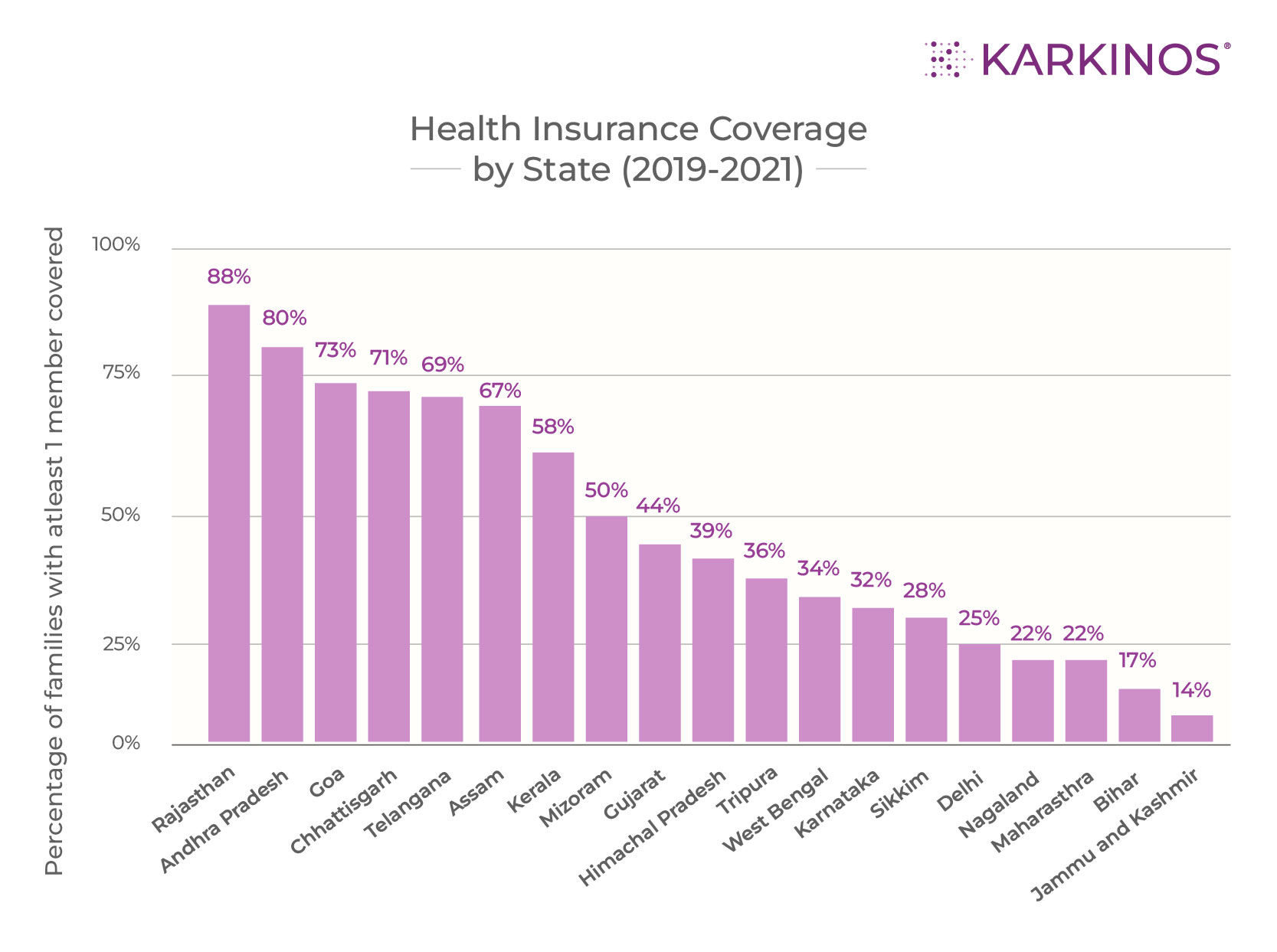

While both public and private healthcare systems exist, limitations in public funding push many towards private insurers, with Maharashtra, Tamil Nadu, and Karnataka leading the way in premium collection. This highlights the urgent need to bridge the gap between rising healthcare costs and accessibility, ensuring more Indians have the peace of mind and financial protection that comes with health insurance.

There are some financial aspects to consider. Government spending on healthcare is gradually increasing but still lags behind developed nations. Out-of-pocket payments have declined yet remain significant at 48% of total healthcare spending. While employer-sponsored health insurance is growing, concerns exist about rising costs.

Sri Sathya Sai Institute of Higher Learning.

Sri Sathya Sai Institute of Higher Learning.